2026-2027 Federal Budget Recap for Business Owners

Jim Chalmers handed down the 2026-27 Federal Budget on 25 March 2026 and if you run a business in Australia, this one’s worth your full attention. Since then, the pace of change hasn’t let up. The core CGT and negative gearing package is now law. The foreign resident CGT rules are before Parliament. The trust minimum tax has a design paper out for consultation. And in June, the High Court handed down a decision that reshaped how trust distributions to companies are treated which is arguably as significant for private groups as anything in the Budget itself.

We’ve updated this recap so you can see exactly where each measure now stands: what’s law, what’s before Parliament, and what’s still just an announcement. *Rubs hands* lets get into it!

Why This Budget Is Different

The 2026 Federal Budget lands in the context of a global oil shock that’s slowed Australia’s economic growth, elevated inflation, and multiple interest rate increases over recent years. The government’s stated aims in this budget are to ease cost-of-living pressure on working Australians in the near term while strengthening the long-term budget position.

For business owners, the proposed changes span income tax, superannuation, and several structural areas – though a number of these remain announced proposals rather than legislated law. Four months on, a good deal of that has now passed into law, though some of the most consequential measures, particularly around trusts, are still working their way through Parliament.

If you want to compare the measures in this Budget against the prior cycle, our 2024 Federal Budget recap covers what was announced and what passed into law from that year.

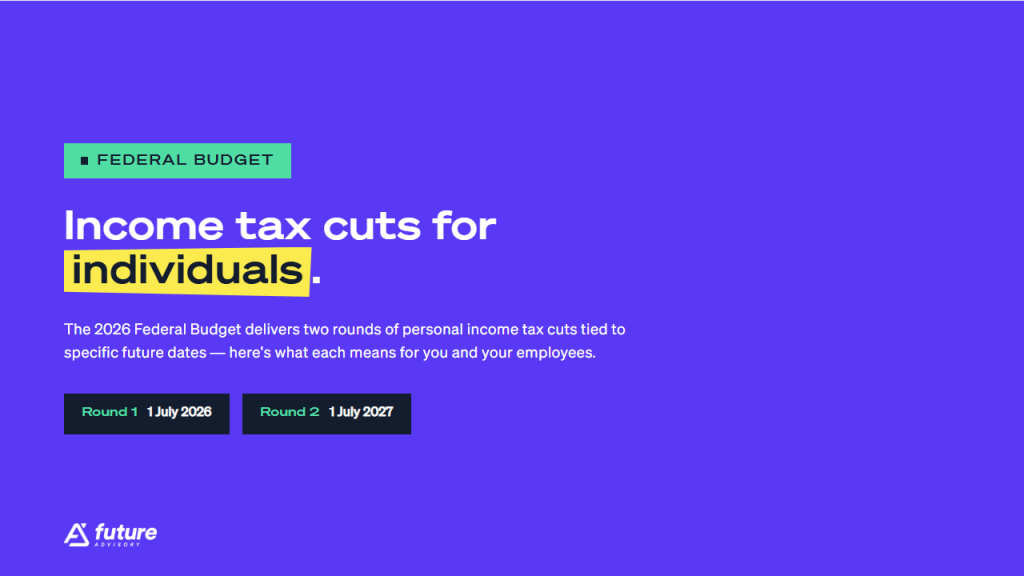

Income Tax Cuts For Individuals

The 2026 federal budget delivers two rounds of personal income tax cuts tied to specific future dates. Both are now part of the same Act that carried the CGT reforms.

From 1 July 2026

The tax rate on income between $18,201 and $45,000 drops from 16% to 15%, saving most workers around $236 per year. A new $1,000 instant work-related tax deduction (no receipts required) also takes effect – a simple win for employees and sole traders alike.

From 1 July 2027

That same rate drops again to 14%, delivering a further $236 saving – a total of $472/year for anyone earning above $45,000. A new Working Australians Tax Offset of $250/year becomes available from the 2027–28 tax return, targeting bracket creep for middle-income earners.

UPDATE

Both the $1,000 standard deduction and the Working Australians Tax Offset were carried in the same Bill as the CGT and negative gearing reforms and are now legislated.

What’s already changed?

Minimum wage: 4.75% increase

- The Fair Work Commission increased modern award rates by 4.75% from the first full pay period on or after 1 July 2026, taking the national minimum to $26.44 per hour

- Award-reliant workers (concentrated in hospitality, retail, administration, and healthcare) are the direct recipients, but the decision tends to set a benchmark across the broader workforce.

- Casual employees at the minimum wage must now receive at least $33.05 per hour, including the 25% casual loading.

Super guarantee: rate rises to 12%

- The SG rate reached 12% on 1 July 2025, the final step in a legislated schedule that has been running since 2021.

- For businesses with ten employees on average wages of $80,000, that’s approximately $4,000 more in super contributions per year.

- Review employment contracts now. Some older agreements express total remuneration as inclusive of super, which can create unintended underpayment risk if not updated.

Payday super: the biggest payroll change in a generation

- From 1 July 2026, super must be paid at the same time as wages rather than not quarterly. Contributions must reach the employee’s super fund within seven business days of each payday.

- From 1 July 2026, employers also calculate super using “qualifying earnings” (QE) rather than the previous “ordinary time earnings” (OTE) — check this has been correctly configured in your payroll software, as it changes what counts toward the SG base.

- This is a fundamental change to cash flow management for many businesses. Previously, quarterly super payments could be held for up to 90 days. Now that buffer is gone.

- The ATO’s Small Business Super Clearing House closed to new users in October 2025 and shut entirely on 30 June 2026. Businesses still using it must have already moved to an alternative clearing house solution.

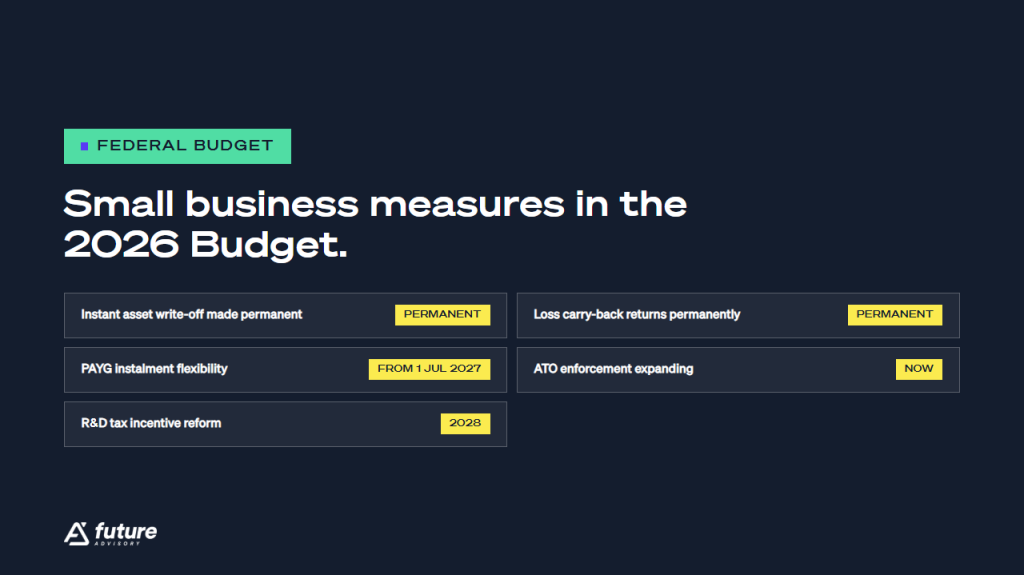

Small Business Measures in the 2026 Budget

Several of the most consequential changes in this federal budget recap are aimed squarely at small business owners. Here’s a breakdown of the key items, including some that require immediate action.

Instant Asset Write-Off Made Permanent

The government has announced that the $20,000 instant asset write-off will be made permanent from 1 July 2026 for businesses with annual turnover under $10 million. Unlike previous years, where the threshold required annual re-legislation, this measure is intended to be an ongoing feature of the tax system if it passes into law. Each eligible asset must cost less than $20,000 and be first used or installed ready for use in the income year you claim the deduction. The government estimates this will improve cash flow for small businesses by around $890 million over five years. This measure has been announced in the Budget but has not yet been legislated.

UPDATE

The above change is before Parliament but has not yet received Royal Assent. Until it passes, the write-off threshold technically reverts to $1,000 from 1 July 2026 under the existing law.

Loss Carry-Back Returns Permanently

The government has announced a proposal to permanently reintroduce loss carry-back provisions for companies with turnover up to $1 billion, proposed to apply from 1 July 2026. Confirm the legislative status of this measure before relying on it for tax planning (it is yet to pass in Parliament). This allows current-year losses to be offset against prior-year profits, resulting in a tax refund.

Quick example:

- FY24/25 profit: $200,000 → company tax paid: $60,000

- FY25/26 loss: $100,000

- Apply the loss → ATO refunds approx. $30,000

- Note: the refund reduces your franking account by the same amount – worth factoring into any dividend strategy

PAYG Instalment Flexibility (From 1 July 2027)

The Budget also announces that businesses will be able to opt into monthly PAYG instalments from 1 July 2027, giving more flexibility to align tax payments with actual cash flow rather than quarterly estimates. If you are not across how the PAYG instalment system currently works, our explainer on PAYG instalments is worth reading ahead of this change.

ATO Enforcement Expanding

Significant funding targets ATO fraud detection, debt recovery, and compliance. Expect expanded garnishee powers and a new joint asset risk provision – meaning the ATO gains greater power to pursue assets held jointly where one party carries an unpaid tax debt. If your business has outstanding obligations, act now.

If your business has outstanding obligations, act now. Understanding your options around ATO compliance and penalty remissions is a practical first step before the ATO’s expanded enforcement powers take effect. It is also worth running through the compliance obligations business owners most commonly miss – particularly around super and BAS, which sit squarely in the ATO’s enforcement focus areas.

R&D Tax Incentive Reform (2028)

From 1 July 2028, the R&D Tax Incentive is being reformed to better target experimental core R&D. The changes include higher offset rates for genuine experimental R&D, an increase in the turnover threshold for the refundable offset to $50 million, and a minimum expenditure threshold of $50,000 for claims. If your business relies on R&D claims, review your current activities against the new eligibility criteria with your adviser ahead of the commencement date. If your business relies on R&D claims, start strengthening your record-keeping now.

Capital Gains Tax Changes – The Biggest Reform in This Budget

This is the section that has changed most since our last update, and the one most business owners need to read carefully. The core CGT reform is no longer a Budget proposal — it has passed Parliament.

Treasury Laws Amendment (Tax Reform No. 1) Act 2026 received Royal Assent on 26 June 2026. This Act legislates the CGT discount replacement, the negative gearing changes below, the $1,000 deduction, the Working Australians Tax Offset, an increase in the small business 50% CGT reduction turnover threshold from $2 million to $10 million (effective 1 July 2027), and a prohibition on SMSFs using limited recourse borrowing arrangements to acquire residential property. These are the law as it stands, not a proposal.

What Changes from 1 July 2027?

The 50% CGT discount for individuals, trusts, and partnerships is replaced with cost base indexation and a minimum 30% tax rate applied to real capital gains. In plain terms: instead of paying tax on only 50% of your gain, the gain is indexed to inflation and taxed at a minimum rate of 30%. For fast-appreciating assets, this generally means a higher taxable amount than under the old regime.

Affected entities include:

- Individuals selling investment assets or business interests

- Trusts distributing capital gains

- Partnerships realising gains on business assets

- Shareholders in private companies held outside of superannuation

The Act also changes the order in which capital losses must be applied. Taxpayers are now required to apply capital losses against discounted capital gains before non-discounted capital gains — reversing the previous position, where taxpayers could choose the order. This affects loss-planning strategies around 30 June.

What’s Still Exempt?

- Your main residence – the family home CGT exemption remains untouched

- For a full breakdown of how the main residence exemption works, including the six-year rule and scenarios for properties that have been rented out, see our guide to the main residence CGT exemption.

- Superannuation funds, including SMSFs, receive a one-third discount on capital gains for assets held over 12 months, resulting in an effective CGT rate of 10%. This existing treatment is not affected by the proposed changes.

- Gains arising before 1 July 2027 still attract the 50% discount, even if the asset is sold later – so the timing of a sale matters

- Small business CGT concessions (15-year exemption, retirement exemption, rollover) remain – though they interact differently under the new regime and should be reviewed with your adviser

- New residential dwellings and affordable housing: owners can choose to retain the existing 50% discount or apply the new indexation framework.

Foreign investors: a more layered picture than “15% vs 30%”

- The 15% figure is the foreign resident capital gains withholding (FRCGW) rate, not a final tax rate. It’s an amount withheld at settlement on Australian property sales involving a foreign vendor (increased from 12.5% to 15% from 1 January 2025, with the previous $750,000 threshold removed so it now applies to all property values). It is a payment on account, not the tax the foreign resident ultimately owes.

- Foreign residents are taxed at a flat rate from the first dollar of Australian-sourced income, with no tax-free threshold (generally a less favourable position than residents face, not a more favourable one).

- The genuine asymmetry sits between foreign investors using MIT (managed investment trust) structures, who can access a concessional final withholding rate around 15% on eligible income, and foreign investors outside MIT structures holding direct Australian real property, who face a minimum 30% tax rate. This distinction predates this Budget but is worth explaining.

- A separate Bill was introduced into the House of Representatives on 2 July 2026. It broadens the statutory definition of “real property” for foreign resident CGT purposes, covering assets with a close economic connection to Australian land and resources such as energy infrastructure, transport assets, and water entitlements. This was originally proposed to apply retrospectively to 12 December 2006 in the exposure draft; that retrospective element has now been removed from the Bill following consultation, so the expanded definition will only apply prospectively from commencement.

- The same Bill includes a time-limited 50% CGT discount for foreign residents disposing of eligible Australian renewable energy assets (battery storage, wind, solar) between commencement and 30 June 2030 — a genuine concessional 15% effective outcome, but only for that narrow category and only foreign companies and trusts (foreign individuals are excluded).

- This Bill is before Parliament and is not yet law. Based on current sitting timetables it could pass in the August 2026 sitting period and commence as early as 1 October 2026 — but that’s not guaranteed.

Pre-CGT Assets – A Valuation Deadline You Cannot Ignore

Pre-CGT assets acquired before 20 September 1985 are currently fully exempt from capital gains tax. If the government’s proposed CGT changes proceed as announced – which is not yet certain – the treatment of post-announcement growth on these assets may change. If you hold pre-CGT assets, this is worth discussing with us once the legislative position is clearer. We will update this article as developments occur.

Pre-CGT asset questions often intersect with estate planning. Our guide to deceased estates and CGT covers the related territory.

New: Innovative Business CGT Concession (announced, not yet legislated)

In response to concerns that the CGT reforms would disproportionately hit entrepreneurial founders holding low-cost-base shares in their own companies, the Government announced on 18 June 2026 that it intends to introduce an “Innovative Business CGT Concession” (IBCC) for founders, employees participating in employee share schemes, and early-stage investors. Detail is still limited and this has not been through an exposure draft.

Negative Gearing Changes (Now Law)

Negative gearing on residential property has been restricted – but existing investors are protected. Here’s the clear breakdown.

What Changes

Residential dwellings acquired after 7:30pm AEST on 12 May 2026 (Budget night), other than new builds, will no longer qualify for full negative gearing treatment from 1 July 2027. Net rental losses from these properties can no longer be deducted against non-rental income such as salary and wages.

What’s Protected

- Properties held at Budget night are fully exempt

- The 50% CGT discount continues for gains arising before 1 July 2027 on these properties

- Losses from negatively geared established properties acquired after Budget night aren’t lost – they’re quarantined and can offset future residential rental income or CGT on eventual sale

- Build-to-rent developments and government housing investments remain exempt

- Commercial property, shares, and other asset classes are completely unaffected

- Where a discretionary trust holds a post-Budget-night residential property, the loss must be utilised within the trust rather than distributed out.

Labor projects 75,000 additional homes will reach the market via these measures, with new builds remaining the most tax-advantaged residential investment path.

Superannuation Changes

- The Superannuation Guarantee (SG) rate reached 12% from 1 July 2025 under the previously legislated schedule. This is already in effect and should already be reflected in your payroll. If you need to confirm your current setup is compliant, speak with our team.

- Employers: review your payroll and employment contracts before 1 July to ensure compliance. If you need help modelling the impact, our team can run the numbers.

- SMSFs are now prohibited from using limited recourse borrowing arrangements (LRBAs) to acquire residential property, following a Greens amendment accepted into the Act now in force. If any client’s SMSF was planning a geared residential property purchase, this needs an urgent conversation

- SMSFs and most super funds are excluded from the new negative gearing restrictions. Existing super tax arrangements and the main residence CGT exemption remain unaffected by the CGT changes.

For employees looking to make the most of their superannuation position, understanding what salary sacrificing means for your super contributions is a good starting point.

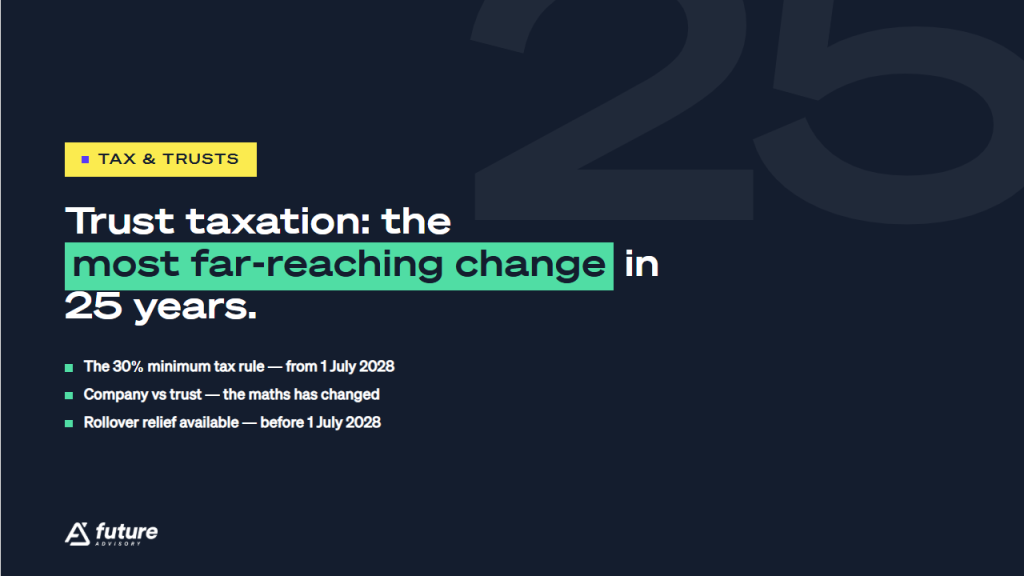

Trust Taxation – The Most Far-Reaching Change in 25 Years

If you are not across how a discretionary trust differs from a unit trust, hybrid trust, or testamentary trust, our guide to the types of trusts in Australia covers the full picture before you read on.

The 30% Minimum Tax Rule (From 1 July 2028)

The government has announced a proposal to apply a minimum 30% tax rate to income distributed through discretionary trusts, with the trustee liable and beneficiaries receiving a non-refundable credit to avoid double taxation. If legislated, this would significantly affect income-splitting strategies used by many family and business trusts. This measure has not yet passed into law. The final form and start date may change.

On 8 July 2026, Treasury released a consultation paper setting out considerably more design detail than was available at Budget time. The consultation period closes 31 July 2026, a very short window, and one advisory bodies have publicly criticised as inadequate for a measure this complex. Key features flagged in the paper:

- Corporate beneficiaries generally will not receive a credit for tax paid by the trustee — this is a deliberate design choice intended to reduce the attractiveness of distributing to a corporate “bucket company” beneficiary, and it interacts directly with the Bendel decision below.

- Franked distributions flowing through a trust are still subject to the 30% trustee-level tax, but the attached franking credit can be used to offset the trustee’s liability.

- Carve-outs flagged include primary production income, certain income of vulnerable minors, amounts already subject to non-resident withholding tax, and testamentary trusts in existence on 12 May 2026.

- A time-limited (three-year) rollover relief window is proposed from 1 July 2027, to help eligible trusts restructure out of the discretionary trust structure before the minimum tax applies.

The measure is estimated to raise around $4.5 billion in receipts over five years — a signal of how seriously the Government intends to pursue it, even though it remains unlegislated.

Company vs Trust – The Maths Has Changed

The company tax rate for base rate entities sits at 25%. If the proposed trust tax changes proceed as announced, the relative merits of company versus trust structures would shift for many businesses. This is worth monitoring closely. We would recommend holding off on any restructuring decisions until the legislation is confirmed, at which point our team can model the impact for your specific situation.

If the announced trust changes proceed, this is the kind of question a business structure review is designed to answer.

Rollover Relief Available (Proposed Window Confirmed, Detail Still Pending)

The government has indicated that rollover relief would be available for eligible trusts restructuring before the proposed commencement date. As this measure has not been legislated, the details, eligibility conditions, and timing may change. We will update this article when the legislation is tabled.

Read our full guide on trust structures in Australia to understand your options.

Excluded from the 30% minimum rule: widely held trusts (including most managed investment trusts) and superannuation funds (including SMSFs).

Bendel: the High Court just overturned 16 years of ATO practice on UPEs

- On 10 June 2026, the High Court handed down its decision in Commissioner of Taxation v Bendel, ruling 5–2 that an unpaid present entitlement (UPE) owed by a trust to a corporate beneficiary is not a loan for Division 7A purposes. This directly overturns the ATO’s position that has governed trust distribution practice since 2010.

- In practical terms, this means that leaving a trust distribution unpaid to a company beneficiary no longer automatically creates a deemed dividend, removing a compliance risk that has shaped how many private groups structure their distributions for over a decade.

- The ATO released its Decision Impact Statement on 26 June 2026. It confirms TR 2010/3 will be withdrawn and other related guidance reviewed, with favourable treatment generally grandfathered for arrangements that began before withdrawal takes effect — but the ATO has been clear that Subdivision EA and section 100A still apply. Subdivision EA can trigger a deemed dividend where a trust with a UPE to a company makes loans or payments to associated parties. Section 100A can apply where trust income is appointed to one beneficiary but enjoyed by another, with the trustee taxed at the top marginal rate as the consequence.

- Bendel is a genuine win for private groups, but it is not a green light to unwind existing UPE loan agreements or sub-trust arrangements without advice — those arrangements remain legally operative and may carry their own tax and commercial consequences if unwound carelessly.

- The window matters here. If the trust minimum tax proceeds broadly as set out in the July consultation paper, corporate beneficiaries lose much of their appeal regardless of Bendel, given they won’t receive a credit for trustee-level tax. That gives private groups roughly a two-year window in which Bendel’s relief is at its most valuable.

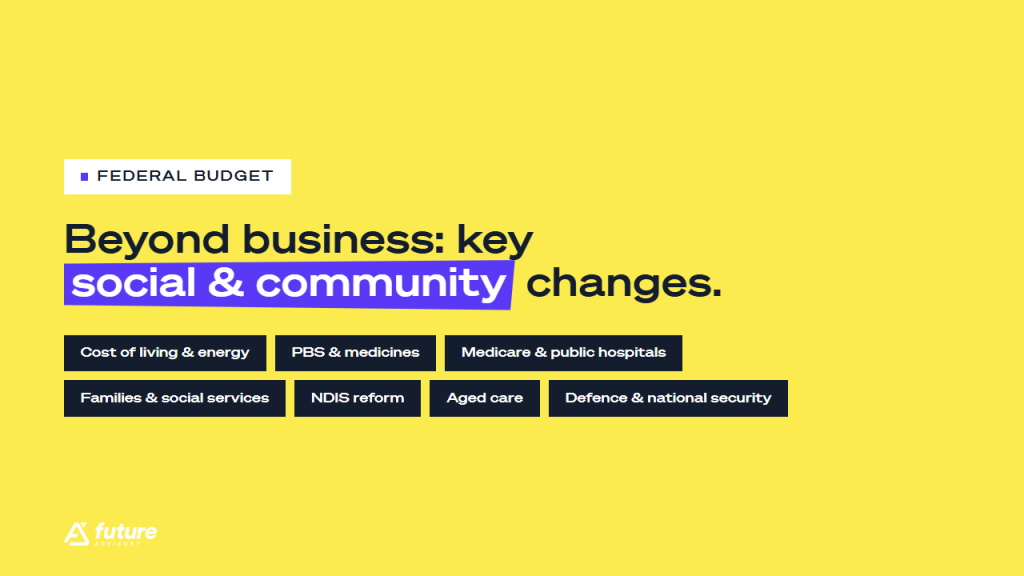

Beyond Business: Key Social & Community Changes

Not every line in the 2026 Federal Budget is aimed at business owners – here’s a summary of the broader community impacts.

Cost of Living and Energy

- The fuel excise was cut by 26.3 cents per litre from 30 March for three months, reducing the cost of a 65-litre tank by approximately $19

- $10 billion has been committed to expand the national fuel stockpile and fund assessment of new fuel refineries to improve energy security

- The Medicare levy low-income threshold has been raised by 2.9%, with singles now exempt up to $28,011 (up from $27,222), and families up to $47,238.

While much of the Budget’s attention falls on tax and business, there are significant changes across health, disability, aged care, defence and social services that will affect many Australians.

PBS and Medicines

- $5.9 billion over five years for new and amended Pharmaceutical Benefits Scheme (PBS) listings, keeping life-saving medicines affordable

- The government says cheaper medicines reforms since 2022 have already saved Australians more than $2.6 billion.

Medicare and Public Hospitals

- $25 billion in additional Commonwealth funding for public hospitals over five years which is three times the increase under the previous agreement

- 137 Medicare Urgent Care Clinics are being made permanent, with $1.8 billion in funding. By July 2026, four in five Australians will be within a 20-minute drive of one

- Growing investment in medical research through the Medical Research Future Fund, rising to $1 billion per year by 2030–31.

Families and Social Services

- Paid Parental Leave increases to a full six months from July 2026

- The 3 Day Guarantee entitles eligible families to three days of subsidised childcare per week

- $316.1 million over five years to support employment programs and improve job seeker outcomes, as unemployment is forecast to rise to 4.5%

- $182.6 million to make the Child Support Scheme safer for women and children.

NDIS Reform

- The government is resetting the NDIS back to its original intent – supporting people with permanent and significant disability – with stricter eligibility and clearer criteria for funded supports

- Plan budgets for social and community participation will be reset, with New Framework Planning delivering more consistent outcomes from April 2027

- $2 billion committed to a new Thriving Kids program to transition children with lower-level needs to community-based services outside the NDIS

- These reforms are expected to save $37.8 billion over the next four years

Aged Care

- $3.7 billion to expand residential aged care beds and improve care quality, including $1.7 billion to incentivise construction of up to 5,000 new beds per year

- $1.4 billion over four years to improve home care affordability, including fully subsidising personal care services (showering, dressing, and personal support)

- Up to 20 new Specialist Dementia Care units and expanded Hospital to Aged Care Dementia Support programs.

Defence and National Security

- $53 billion in additional defence spending over the next decade, including the $12 billion Henderson Defence Precinct shipyard in Western Australia

- $863.8 million over four years for the nuclear-powered submarine program under AUKUS

- Almost $800 million for veterans, including $583.4 million to implement recommendations from the Royal Commission into Defence and Veteran Suicide.

But What Didn’t The Budget Touch On? Revisited.

With the budget always comes long, speculative lists from armchair (and actual) experts about what it will touch on. Here’s what wasn’t in the budget…

Four months on, a couple of items on the original list need an asterisk.

Division 7A Reform

No legislative fix to Division 7A generally was announced, and that’s still true. But it’s worth reading this alongside the Bendel decision above — case law, not the Budget, has done more to reshape Division 7A’s practical operation this year than anything Parliament has passed. The 30% minimum tax on discretionary trusts, if it proceeds, would add further pressure by making the corporate beneficiary strategy less attractive regardless of Division 7A risk.

Individual And Company Tax Residency Rules

Reform of the residency tests for both individuals and companies has been flagged repeatedly. It didn’t make the cut this time.

CGT Rollovers And Demerger Relief

A review of the available rollovers, including demerger rollover relief, remains outstanding, leaving gaps for businesses looking to restructure cleanly.

Small Business CGT Concessions

The Act that received Royal Assent on 26 June 2026 lifts the turnover threshold for the small business 50% active asset reduction from $2 million to $10 million from 1 July 2027 — a genuine widening of access, even if the core concessions themselves weren’t otherwise simplified.

Section 100A And Trust Reimbursement Agreements

Further guidance or legislative clarity on the ATO’s approach to section 100A had been anticipated. Again, nothing, though the trust taxation changes may quietly reduce some of its relevance over time.

Family Trust Distribution Tax Rules

Known deficiencies in the rules have been flagged by advisers for years. They remain unaddressed.

There’s a lot of change in this Federal Budget, and plenty of those changes will directly affect our clients. If any of the above has you feeling like you need to touch based, please do!

2026 Federal Budget Glossary

A quick reminder on what some of the above terms actually mean…

- Loss carry-back: When a business that made a profit in a previous year can offset a current-year loss against that profit to claim a tax refund.

- Bracket creep: When wage growth pushes people into higher tax brackets over time, even if their purchasing power hasn’t actually increased.

- Cost-based inflation: When prices rise because the cost of producing goods and services increases, driven by things like wages, energy, or supply chain pressures, rather than excess demand.

- Negative gearing: When the costs of owning an investment (like loan interest and maintenance) exceed the income it earns, creating a loss that can be offset against other taxable income.

- Capital gains tax: A tax on the profit made when you sell an asset (like property or shares) for more than you paid for it.

- Super guarantee: The minimum percentage of an employee’s earnings that employers are legally required to contribute to their superannuation fund.

- Discretionary trust: A legal structure where a trustee has the flexibility to decide how income and assets are distributed among beneficiaries each year.

- Widely held trust: A trust with a large number of beneficiaries or unit holders (typically managed funds or listed trusts) subject to different tax rules than discretionary trusts.

- Medicare levy: A compulsory contribution (currently 2% of taxable income) paid by most Australian taxpayers to help fund the public health system.

- PBS (Pharmaceutical Benefits Scheme): A government program that subsidises the cost of a wide range of medicines for Australians, making them more affordable at the pharmacy.

- Paid parental leave: A government-funded payment to eligible parents taking time off work following the birth or adoption of a child, designed to support families during that period.

- Franking account: A record kept by a company tracking the tax it has already paid on its profits, which can be passed on to shareholders as franking credits to avoid being taxed twice on the same income.

What Should You Do Now?

The 2026-2027 federal budget is one of the most structurally significant in recent memory for Australian business owners. Capital gains tax, trust distribution rules, and super all shift – and some of those shifts have hard deadlines.

Act now – these are already legislated and in effect

The Superannuation Guarantee rate reached 12% on 1 July 2025. If you have not already confirmed your payroll reflects this, check it immediately.

The Stage 3 income tax cuts are legislated and apply from 1 July 2026. If you run payroll, confirm your withholding tables are updated before the next pay run.

Announced in the 2026-27 Budget – not yet legislated, but officially confirmed as government policy

The $20,000 instant asset write-off is announced as permanent from 1 July 2026. If you have been holding off on eligible equipment under $20,000, this measure provides a stable planning window – though we recommend confirming the legislative status with us before committing to timing decisions.

Loss carry-back is announced as returning from 2026-27, allowing eligible companies to offset current losses against tax paid in the prior two income years. If your business made a profit last year and is facing a loss this year, speak with us about whether this applies to your situation.

The CGT reform – replacing the 50% discount with inflation-based indexation and a 30% minimum rate – is announced to apply to gains arising from 1 July 2027 onwards. If you are planning to sell a business asset, shares, or investment property, bring that conversation forward. The timing of a sale relative to 1 July 2027 could be material – but only if this measure is legislated. We will keep you updated.

Negative gearing restrictions on established residential property acquired after Budget night are announced to apply from 1 July 2027. If you are considering purchasing investment property, speak with us before proceeding.

The 30% minimum tax on discretionary trust distributions is announced to apply from 1 July 2028, with three years of rollover relief available from 1 July 2027 for businesses that restructure. If your business operates through a discretionary trust, this is worth discussing with us now on a planning basis – not to restructure immediately, but to understand your options if the measure is legislated.

One important note on all Budget measures above

Announced Budget measures reflect government policy intent. They are not law until passed by Parliament. Some measures may be amended, delayed, or not proceed. We will update this article as legislation progresses.

Future Advisory is a Melbourne-based accounting firm working with small business owners, tradies, and growing companies across Australia. Our accounting and tax services cover everything from business structure reviews to CGT planning and trust advice. If this federal budget recap has raised questions about your situation, we would love to help you work through them.